All Categories

Featured

Table of Contents

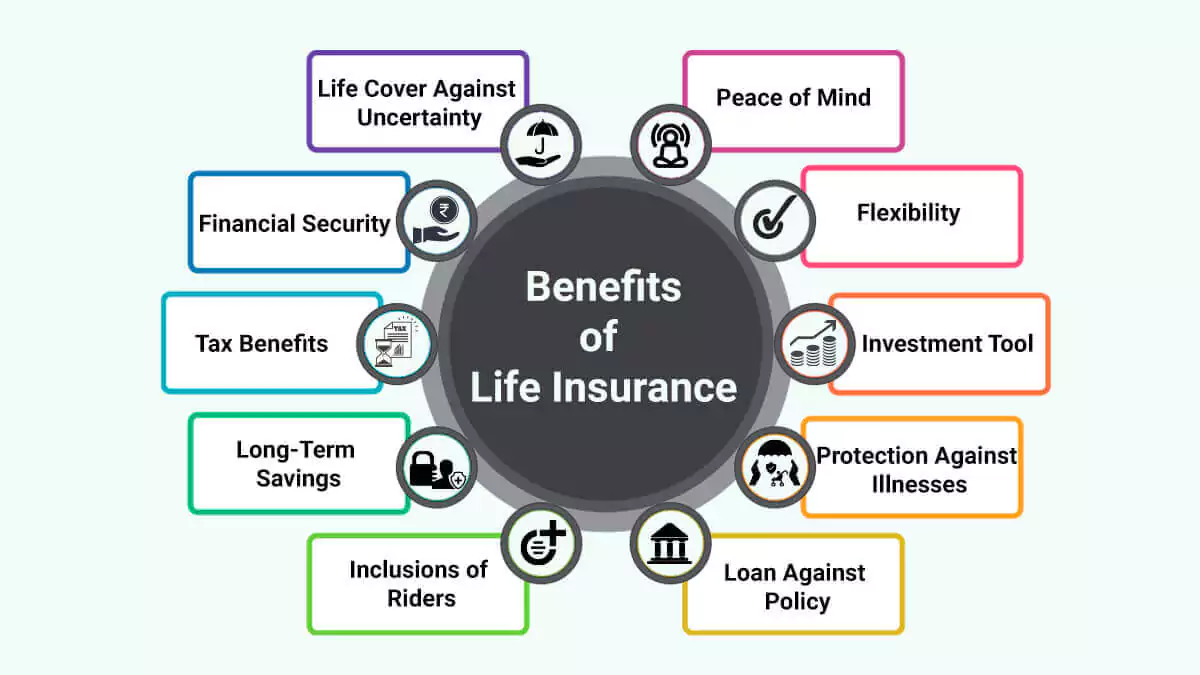

Life insurance policy offers five economic benefits for you and your family members. The main advantage of adding life insurance to your monetary plan is that if you die, your successors obtain a swelling sum, tax-free payment from the policy. They can utilize this cash to pay your last costs and to replace your revenue.

Some plans pay out if you develop a chronic/terminal illness and some provide savings you can use to sustain your retirement. In this post, discover the various benefits of life insurance and why it may be a great concept to spend in it. Life insurance coverage supplies benefits while you're still to life and when you die.

How do I apply for Accidental Death?

Life insurance payouts generally are income-tax free. Some permanent life insurance plans develop cash value, which is cash you can take out while still to life.

If you have a policy (or policies) of that size, individuals that depend upon your earnings will certainly still have money to cover their continuous living costs. Beneficiaries can use policy advantages to cover important everyday expenditures like rent or mortgage payments, energy expenses, and groceries. Average annual expenditures for houses in 2022 were $72,967, according to the Bureau of Labor Data.

Life insurance payments aren't taken into consideration earnings for tax objectives, and your beneficiaries do not have to report the cash when they submit their tax returns. Depending on your state's regulations, life insurance benefits may be utilized to offset some or all of owed estate tax obligations.

Development is not affected by market problems, allowing the funds to collect at a secure price over time. Additionally, the cash value of whole life insurance policy grows tax-deferred. This suggests there are no income tax obligations built up on the money value (or its growth) until it is taken out. As the cash worth develops over time, you can use it to cover costs, such as getting a cars and truck or making a down repayment on a home.

Guaranteed Benefits

If you determine to obtain against your money value, the car loan is not subject to revenue tax as long as the plan is not given up. The insurance firm, nevertheless, will bill rate of interest on the loan quantity till you pay it back. Insurance provider have varying rate of interest on these finances.

For instance, 8 out of 10 Millennials overestimated the expense of life insurance policy in a 2022 research study. In reality, the ordinary price is better to $200 a year. If you think buying life insurance policy might be a wise financial move for you and your family, think about speaking with a financial expert to embrace it right into your monetary plan.

What should I know before getting Universal Life Insurance?

The 5 primary types of life insurance policy are term life, entire life, universal life, variable life, and last expense insurance coverage, additionally called funeral insurance coverage. Each type has various functions and advantages. Term is more affordable yet has an expiration day. Entire life starts costing a lot more, yet can last your entire life if you keep paying the premiums.

It can settle your debts and medical expenses. Life insurance policy could likewise cover your mortgage and supply cash for your family to keep paying their bills. If you have family relying on your revenue, you likely require life insurance policy to sustain them after you pass away. Stay-at-home moms and dads and local business owner additionally typically require life insurance policy.

Minimal amounts are offered in increments of $10,000. Under this strategy, the chosen coverage takes impact 2 years after enrollment as long as premiums are paid throughout the two-year duration.

Insurance coverage can be prolonged for up to two years if the Servicemember is totally impaired at separation. SGLI protection is automatic for most energetic responsibility Servicemembers, Ready Book and National Guard members set up to perform at the very least 12 periods of non-active training per year, participants of the Commissioned Corps of the National Oceanic and Atmospheric Administration and the Public Health Service, cadets and midshipmen of the United state

VMLI is available to Readily available who experts that Got Adapted Particularly Adjusted Real EstateGive), have title to the home, and have a mortgage on the home. All Servicemembers with full-time insurance coverage need to use the SGLI Online Registration System (SOES) to designate beneficiaries, or decrease, decrease or restore SGLI coverage.

Participants with part-time insurance coverage or do not have accessibility to SOES must use SGLV 8286 to make adjustments to SGLI (Estate planning). Full and documents form SGLV 8714 or look for VGLI online. All Servicemembers should use SOES to decline, reduce, or recover FSGLI coverage. To access SOES, go to www.milconnect.dmdc.osd.mil/milconnect/. Members who do not have accessibility to SOES ought to use SGLV 8286A to to make adjustments to FSGLI protection.

What is included in Death Benefits coverage?

Plan benefits are lowered by any type of outstanding lending or loan rate of interest and/or withdrawals. Returns, if any, are impacted by plan financings and finance interest. Withdrawals above the price basis might result in taxable normal earnings. If the plan gaps, or is surrendered, any kind of outstanding loans considered gain in the plan may undergo common revenue tax obligations.

If the plan owner is under 59, any type of taxable withdrawal may likewise be subject to a 10% federal tax obligation penalty. All whole life insurance plan warranties are subject to the prompt repayment of all called for costs and the insurance claims paying capacity of the releasing insurance company.

The cash money abandonment worth, lending value and fatality earnings payable will be reduced by any lien impressive as a result of the repayment of a sped up benefit under this rider. The accelerated advantages in the first year show deduction of a single $250 management fee, indexed at a rising cost of living rate of 3% annually to the price of velocity.

A Waiver of Costs cyclist waives the responsibility for the insurance policy holder to pay further costs must she or he become absolutely impaired continuously for a minimum of six months. This rider will certainly sustain an extra price. See plan agreement for extra details and needs.

What is Living Benefits?

Discover more concerning when to get life insurance. A 10-year term life insurance policy policy from eFinancial prices $2025 each month for a healthy grownup that's 2040 years of ages. * Term life insurance is extra economical than long-term life insurance coverage, and women customers usually get a lower price than male consumers of the exact same age and wellness status.

{kind=link}

Latest Posts

Senior Care Usa Final Expense Insurance Reviews

Insurance Funeral Plans

Metlife Term Life Insurance Instant Quote